What We Found

When we started analyzing Web3 M&A data for 2024-2025, we weren't expecting Solana ecosystem companies to stand out quite this much. But the numbers tell a pretty clear story: out of 370 Web3 acquisitions we tracked, 76 involved Solana ecosystem companies—that's about 1 in 5 deals!

What's interesting isn't just the total number, but how the pattern evolved over time. Let's walk through what the data shows.

The Growth Pattern

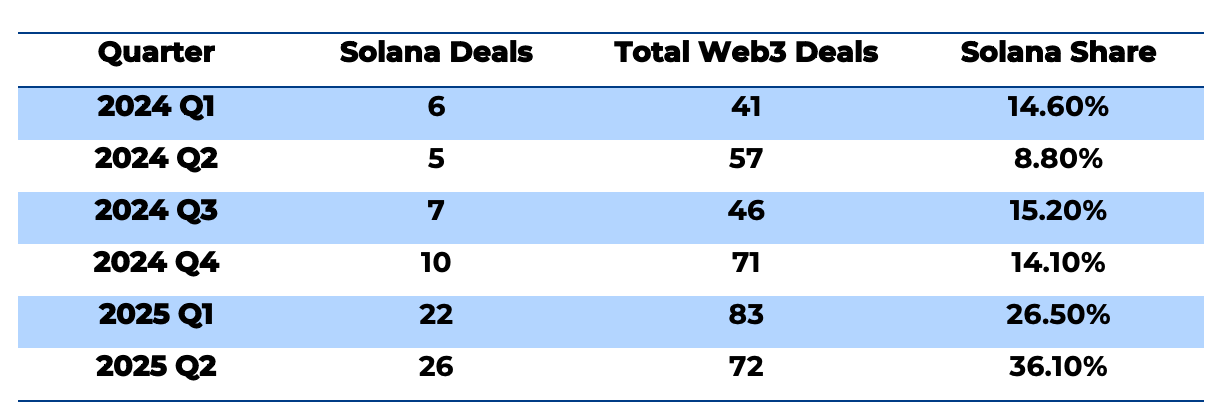

Here's what happened quarter by quarter:

The shift is pretty dramatic. Through most of 2024, Solana deals hovered around 14-15% of the total market. Then something changed in 2025—the share jumped to over 25% in Q1 and kept climbing to 36% in Q2.

Looking at the raw numbers, Solana went from 28 deals in all of 2024 to 48 deals in just the first six months of 2025. That's not just growth—that's acceleration.

Where These Deals Are Happening

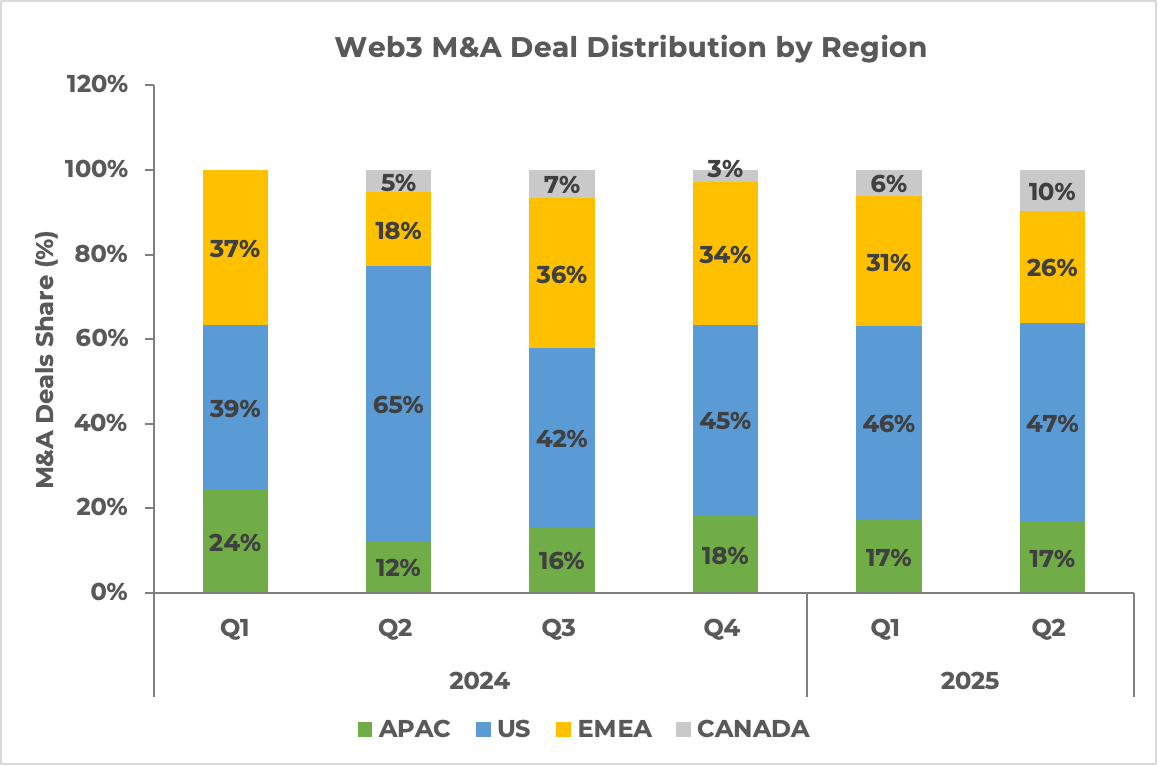

The chart shows the regional distribution of Web3 M&A deals from Q1 2024 to Q2 2025. The US consistently led in deal share, peaking at 65% in Q2 2024 and staying strong at 47% by Q2 2025. EMEA’s share fluctuated throughout the period, reflecting an uneven pace of activity across the region. APAC saw a gradual decline from 24% to 17%, while Canada’s presence, though small, grew steadily to 10%.

These trends highlight the US’s dominance, Canada’s rising role, EMEA’s volatility, and a relative slowdown in APAC.

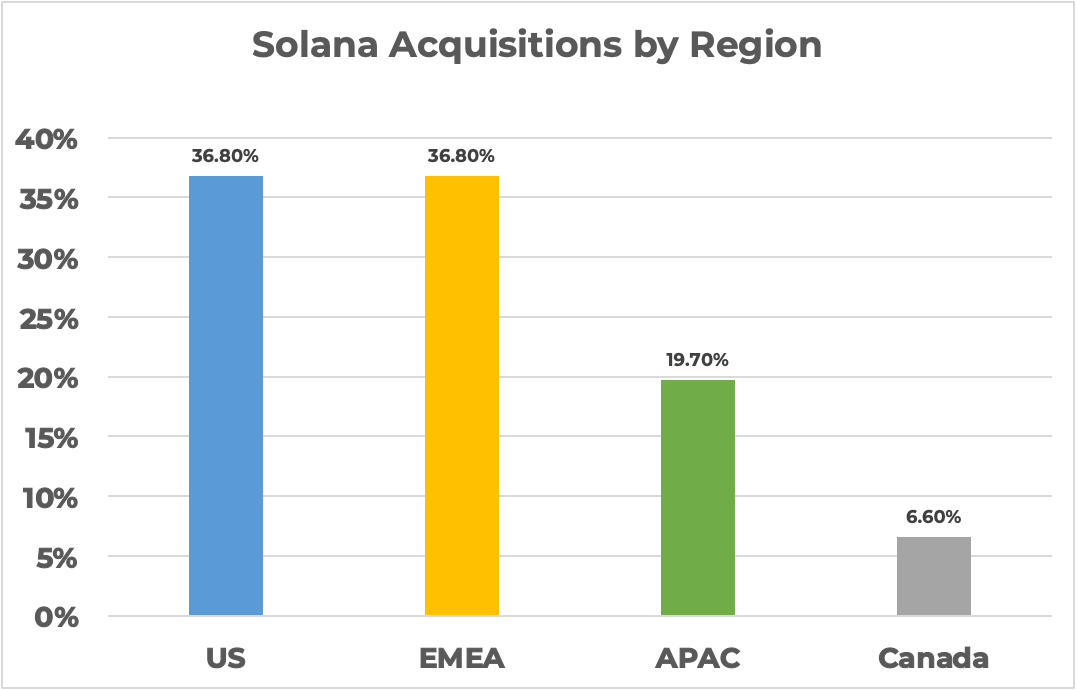

One thing that surprised us was how geographically distributed these acquisitions were:

US: 28 deals (36.8%)

EMEA: 28 deals (36.8%)

APAC: 15 deals (19.7%)

Canada: 5 deals (6.6%)

The US-EMEA split being exactly even suggests this isn't just Silicon Valley enthusiasm. European/UAE companies are acquiring Solana teams at the same rate as American ones, which indicates broader international recognition of the technology and teams.

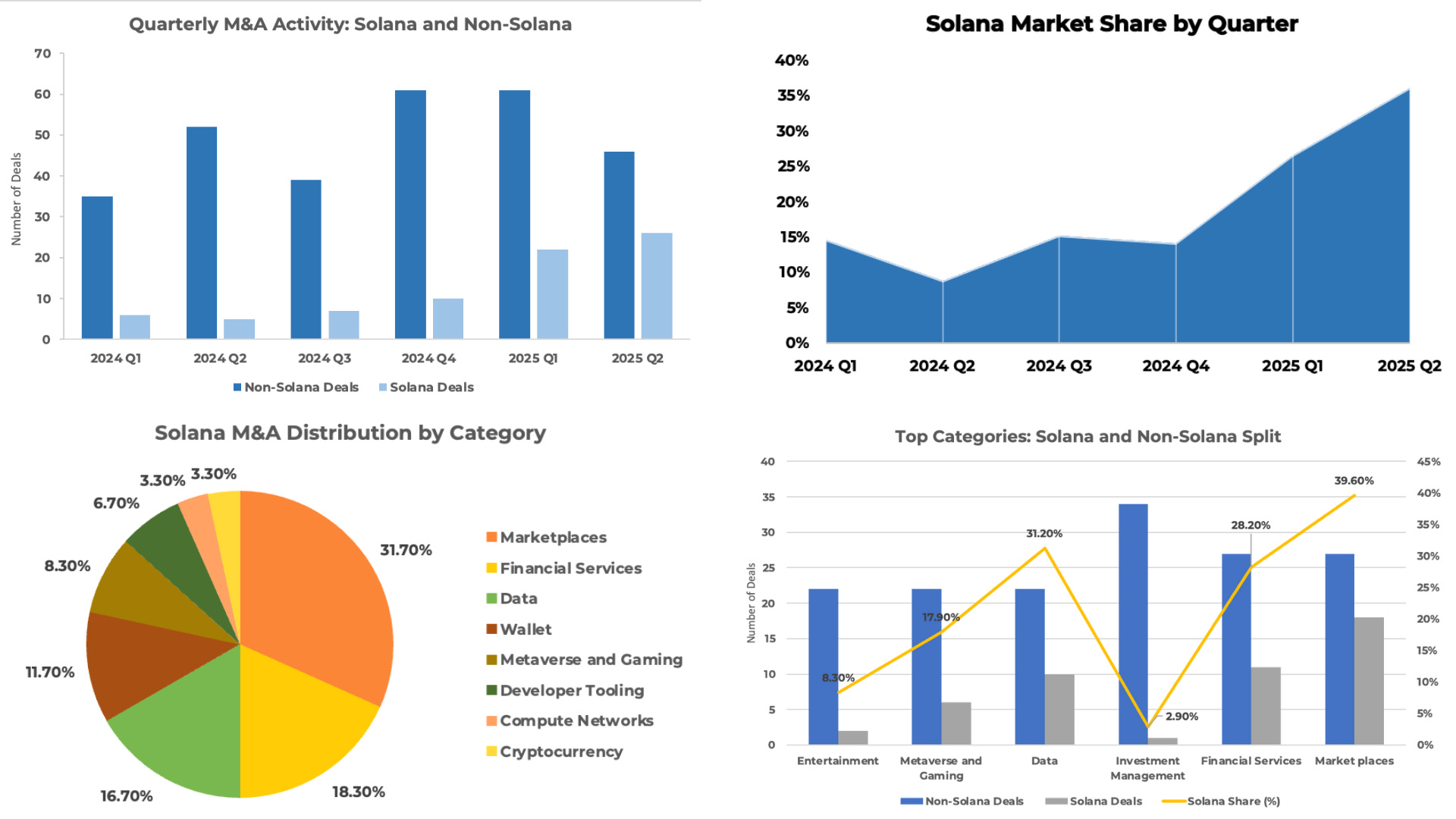

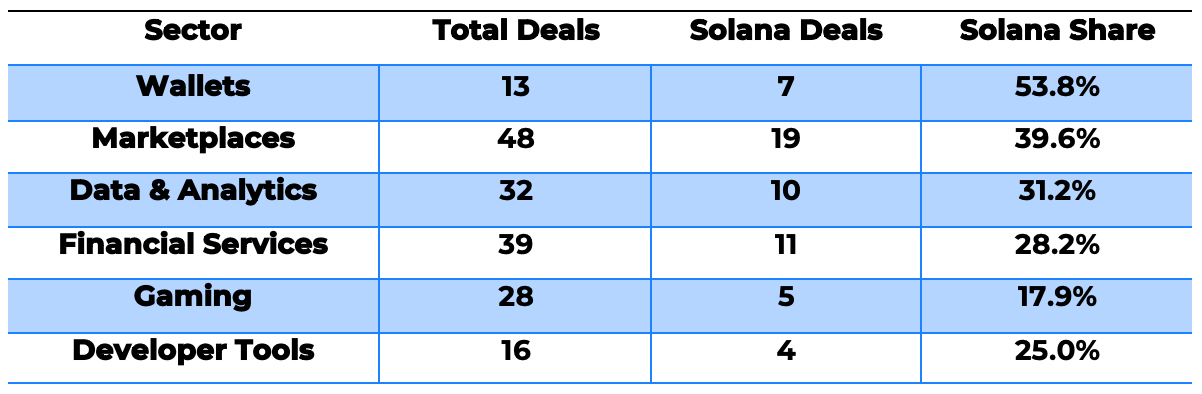

Looking at market share by sector, one number stands out: Solana teams accounted for over half of all wallet acquisitions. That's significant because wallets are often the first point of contact between users and crypto. If acquirers are betting on Solana wallet teams, they're betting on user experience.

The marketplace share is also noteworthy. At nearly 40%, it suggests that when companies want to build or acquire trading infrastructure, they're finding value in what Solana teams have built.

What's also interesting in the financial services category is how many acquisitions involve payment and stablecoin infrastructure. Of the 11 Solana financial services deals, several involve traditional payment companies acquiring teams that built on Solana specifically for its cost and speed advantages in payment processing.

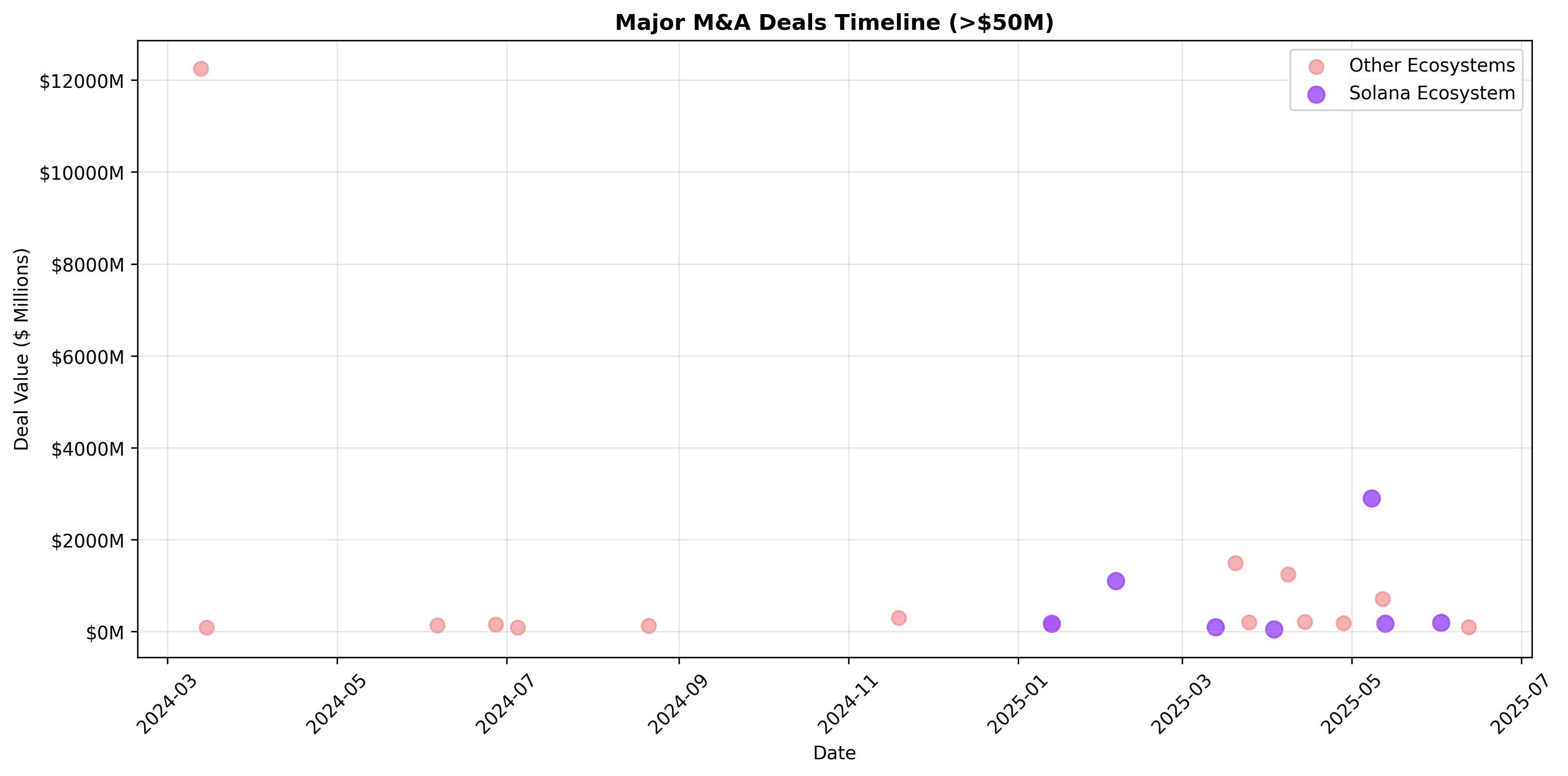

Some Notable Deals

A few acquisitions really illustrate the trend. Stripe made two major moves in 2025 that caught our attention.

Stripe → Bridge ($1.1B, February 2025) [Source: Coindesk]

Bridge wasn't a household name, but they'd built infrastructure that companies like SpaceX and Coinbase were actually using for stablecoin payments. When Stripe paid $1.1 billion for them, it wasn't speculative—Bridge was already processing real transactions for real companies.

What made this interesting from a Solana perspective is that Bridge had built much of their infrastructure to take advantage of Solana's cost and speed characteristics. Stripe wasn't just buying crypto infrastructure; they were buying infrastructure optimized for the kind of high-volume, low-cost transactions that Solana enables.

Stripe → Privy (June 2025) [Source: Coindesk]

Four months later, Stripe acquired Privy, which had built embedded wallet technology for apps. Privy's approach was notable because they'd focused on making crypto onboarding invisible—users could interact with blockchain apps without even knowing they were using crypto wallets.

Again, the Solana connection mattered. Privy had built their system to work across chains, but their best user experiences leveraged Solana's speed for instant transactions and low fees for microtransactions.

Coinbase → Deribit ($2.9B, May 2025)[Source: Coindesk]

The Deribit acquisition was the largest crypto M&A deal we tracked. Coinbase paid $2.9 billion for a derivatives exchange that dominated options trading outside the US. While Deribit operates across multiple chains, their success in handling high-frequency, low-latency trading made Solana infrastructure particularly relevant to their operations.

What's Driving This?

Looking at the acquisition motivations, we identified a few key patterns:

Infrastructure Consolidation (45% of deals): Most acquisitions seem focused on companies that have built foundational infrastructure—payment rails, trading systems, wallet technology. Acquirers appear to be betting that crypto is moving from experimental to utility, and they want to own the pipes.

Technical Expertise (25% of deals): A significant portion of deals look like talent acquisitions. Companies are buying teams that have proven they can build high-performance blockchain applications. The Rust programming skills that Solana development requires are highly transferable to other types of systems.

Market Expansion (20% of deals): Some acquisitions are clearly about geographic expansion or entering new market segments. Companies use acquisitions to quickly gain expertise in markets where they don't have an organic presence.

User Base Consolidation (10% of deals): A smaller portion involves companies acquiring user bases, particularly in gaming and social applications where network effects matter.

The Mobile Factor

One pattern we noticed, particularly in wallet and consumer application acquisitions, is how many Solana teams had prioritized mobile from the beginning. While other ecosystems retrofitted mobile experiences, many Solana teams built mobile-first.

This shows up in the acquisition patterns. Companies acquiring consumer-facing crypto infrastructure often chose Solana teams specifically because they'd solved mobile user experience challenges that other teams were still working on.

Cross-Ecosystem Interest

What's particularly interesting is how many non-Solana companies are acquiring Solana expertise:

ConsenSys (Ethereum-focused) acquired Web3Auth [Source: ConsenSys]

Alchemy (multi-chain infrastructure) acquired DexterLab [Source: The Block]

Stripe (traditional fintech) acquired both Privy and Bridge

MoonPay (crypto payments) acquired Iron [Source: The Block] and Helio [Source: The Block]

This suggests that even companies not primarily focused on Solana recognize that the teams building there have developed valuable expertise and technology that transfers to other contexts.

The TradFi Payments Connection

Looking at these acquisitions more closely, there's a clear pattern around payments infrastructure. Traditional financial companies are specifically targeting Solana teams that have built stablecoin and payment solutions:

Stripe's Strategic Focus: Both Bridge (stablecoin infrastructure) [CNBC] and Privy (embedded wallets) [CoinDesk] solve different pieces of the payments puzzle. Bridge handles the backend payment rails, while Privy handles user onboarding and authentication.

MoonPay's Expansion: Iron (banking infrastructure, $100M+) [PYMNTS] and Helio (payment processing, $175M) [Cointelegraph] represent MoonPay building out a complete payment stack using Solana expertise.

The common thread is that these traditional payment companies recognize Solana's advantages for cost-effective, real-time payment processing. They're not acquiring Solana teams for the blockchain technology itself, but for the payment infrastructure expertise these teams have developed.

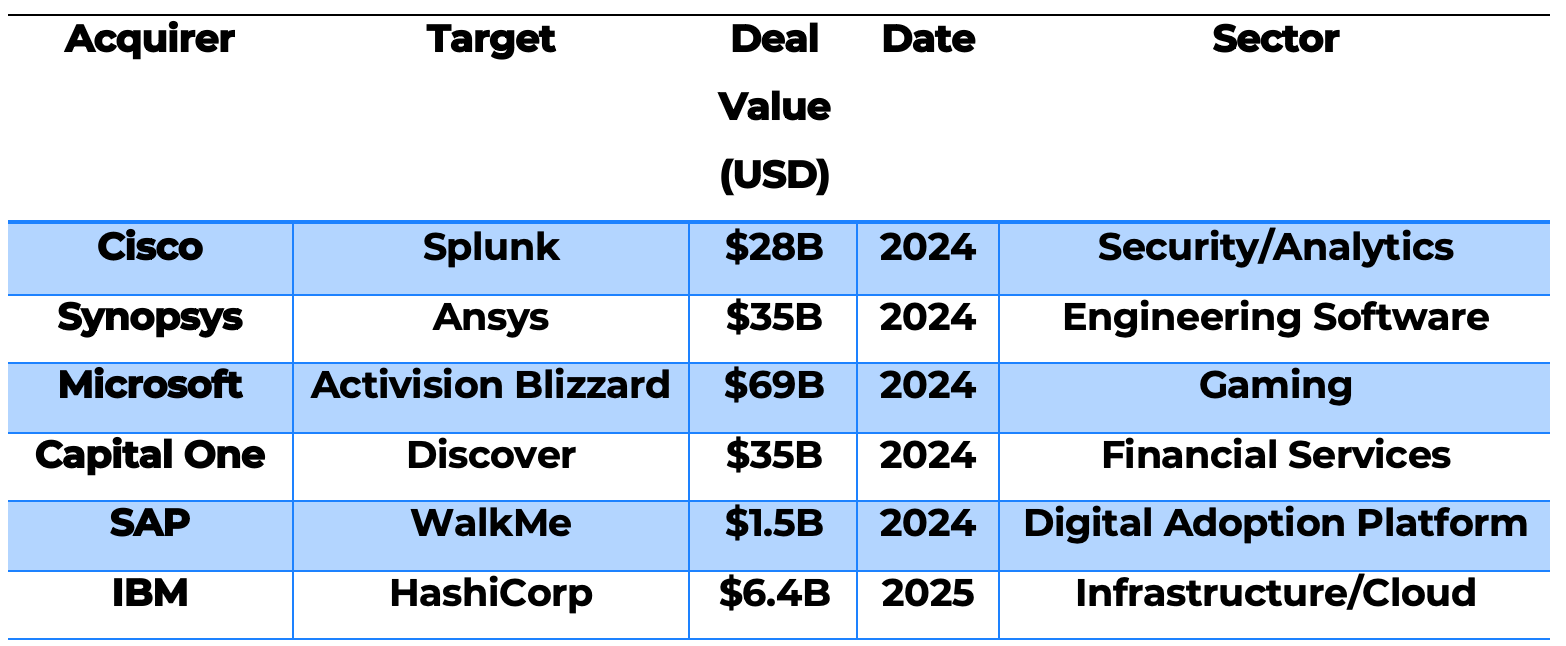

Web2 vs Web3 M&A Context

To put these Web3 numbers in perspective, let's look at what was happening in traditional tech M&A during the same period:

What's interesting is the pattern alignment. While Web2 deals focused heavily on AI/ML capabilities, cloud infrastructure, and user acquisition, Web3 deals show similar themes but in a blockchain context—payment infrastructure, user onboarding (wallets), and data analytics.

The Solana ecosystem's 171% growth rate actually mirrors broader tech M&A trends, where companies are aggressively acquiring specialized technical expertise rather than just user bases. Just as traditional tech companies paid premium valuations for AI and cloud capabilities, Web3 acquirers are paying for blockchain-native infrastructure and the teams who built it.

Notably, some of the largest Web3 deals we tracked (Stripe→Bridge at $1.1B, Coinbase→Deribit at $2.9B) are approaching the scale of mid-tier traditional tech acquisitions, suggesting the space is maturing toward mainstream M&A valuations.

Looking Ahead

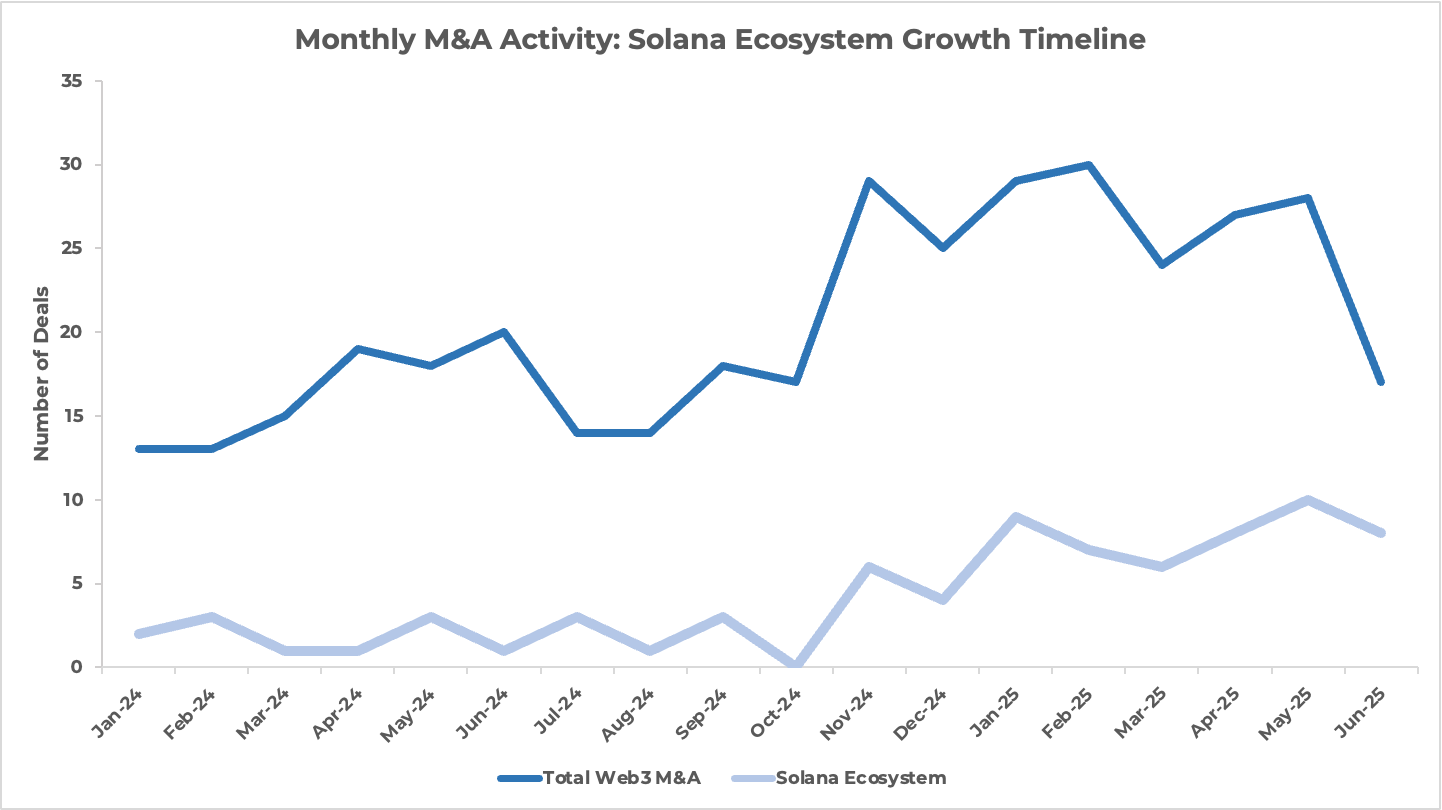

The monthly timeline reveals an unmistakable acceleration pattern. Through most of 2024, Solana ecosystem deals were averaging 2-3 per month. But starting in late 2024, something shifted. By early 2025, we're seeing months with 8-10 Solana deals, representing a clear inflection point in acquisition activity.

What's particularly striking is that this isn't just seasonal variation—the growth appears sustained rather than cyclical. If the current trajectory continues, 2025 could see Solana ecosystem deals reaching 25-30% of the total Web3 M&A market by year-end.

What This Means

The data suggests that Solana ecosystem companies are being acquired not just because they're building interesting crypto applications, but because they're building infrastructure and developing expertise that has value beyond crypto-specific use cases.

The 171% growth rate from 2024 to 2025, the geographic distribution, and the cross-ecosystem interest all point to the same conclusion: these teams are building technology and developing skills that mainstream companies find valuable.

Whether this trend continues will largely depend on whether the teams being acquired can successfully integrate their technology and expertise into larger organizations. But the acquisition activity suggests that buyers believe the technology and talents coming out of the Solana ecosystem are ready for mainstream deployment.

Data Notes

This analysis is based on 370 Web3 M&A deals tracked through Messari's database, cross-referenced with Crunchbase, CoinDesk, and public announcements. We classified companies as "Solana ecosystem" based on where their core technology was developed and their primary blockchain integration.

Deal values were included where publicly disclosed, but many transactions involve undisclosed consideration, so financial analysis should be considered incomplete.

Complete dataset and sources available here: Web3 M&A Data Collection